Reporting obligations for foreign engagements

§§ Sections 138 et seq. AO regulate reporting obligations that also affect the foreign engagement of domestic taxpayers.

Reporting obligations for fiduciary arrangements (Panama Papers)

- § Section 138 II AO regulates reporting obligations for foreign offshore accounts held via trust structures and the like. Keyword: Panama Papers

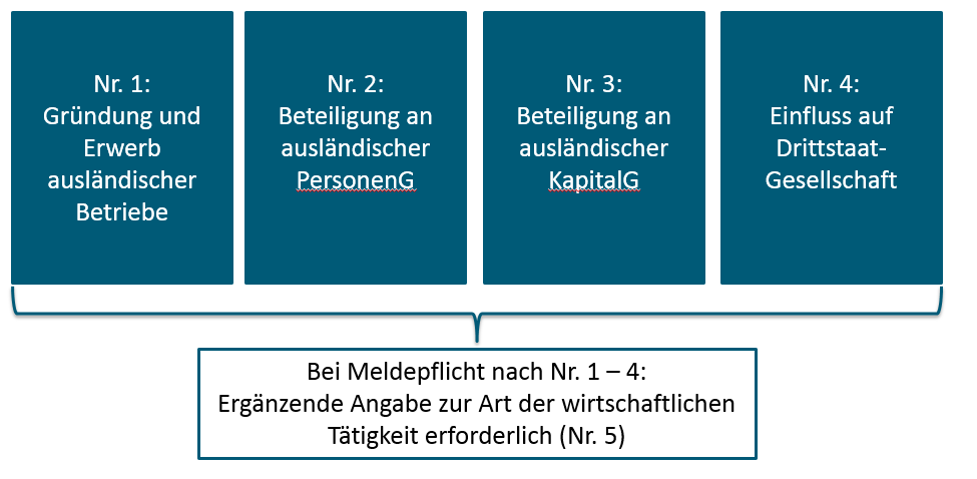

- § Section 138 II 1 No. 4, III AO: Third country offence:

- (2)¹ Taxpayers [...] shall disclose:

- 4. the fact that they, alone or together with related persons within the meaning of section 1(2) of the Foreign Tax Act, may for the first time directly or indirectly exercise a controlling or determining influence over the corporate, financial or business affairs of a third country company; [...].

- (3) A third-country company is a partnership, corporation, association of persons or estate with its seat or management in states or territories which are not members of the European Union or the European Free Trade Association.

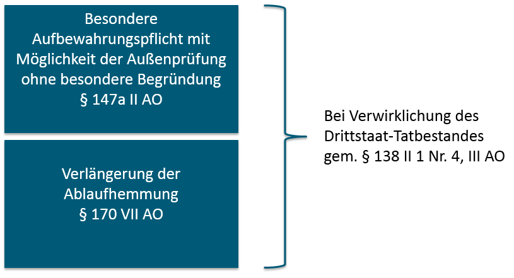

Legal consequences for a third-country company

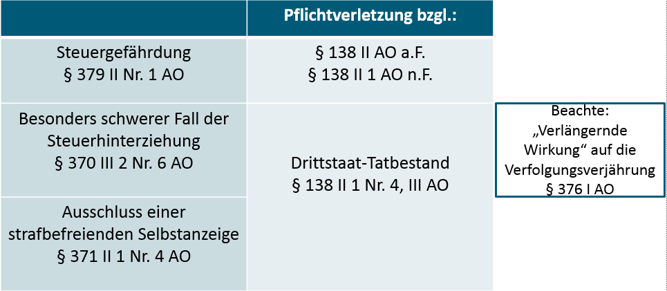

Legal consequences of breach of duty

Reporting obligations in the case of legal tax structuring with a foreign connection

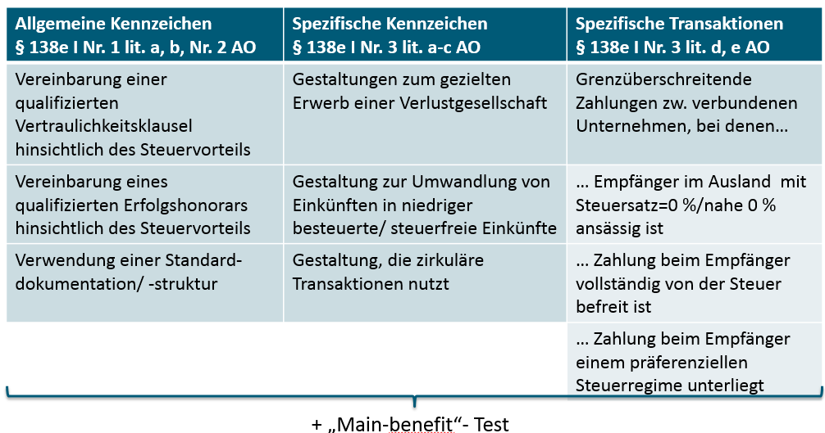

§§ Sections 138 d et seq. of the German Fiscal Code (AO) regulate reporting obligations for legal arrangements with a foreign connection and certain hallmarks. Both the taxpayer and the tax advisor/tax lawyer (so-called intermediary) are obliged to report.

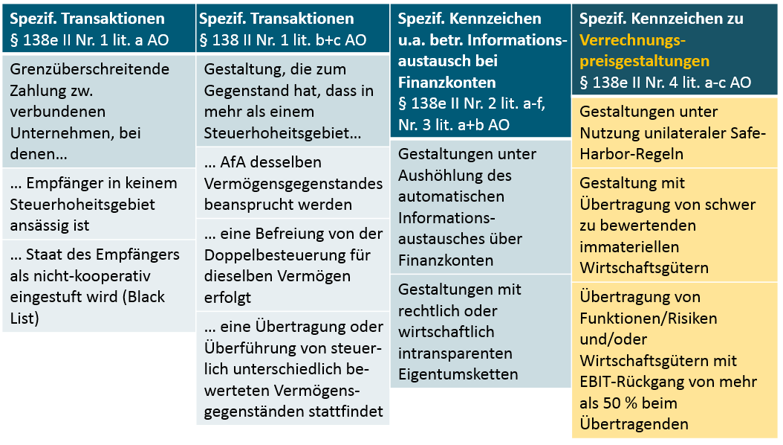

§ Section 138d para. 1 no. 3 lit. a) AO => conditional hallmarks within the meaning of section 138e para. 1 AO

§ 138d para. 1 no. 3 lit. b) AO => unconditional hallmarks within the meaning of § 138e para. 2 AO

Your contact person:

Prof. Dr. Christian Jahndorf

attorney, extraordinary professor Universität Münster (Münster)

Tel.: +49 (0) 2 51/28 08-153

Prof. Dr. iur. Till Zech, LL.M.

Attorney at Law (NY), tax consultant, of counsel Münster

Tel.: +49 (0) 2 51/28 08-0

Master of Science

Dorothee Maasmann

Tax consultant Münster